A New Era For Model Portfolios Powered by Big Data & AI

Authored by: Erez Katz

For over seven years now, we’ve been on a mission to build a platform that can efficiently validate and deploy big data for successful investment. Our goal was two fold:

- For Data Providers: Enable data providers with an empirical and defensible validation of their data. Help them target a new set of consumers who are not looking for the raw data but rather for “fully baked” actionable insights in the form of model portfolios.

- For Asset Managers: Serve asset managers with a wide array of uncorrelated portfolios powered by machine learning and AI. Each portfolio is carefully crafted and scientifically validated both historically and perpetually.

Over the years, we’ve been able to grow our data partnerships and bring to market quite an extensive set of thematic portfolios, all available for consumption on our platform, QuantDesk. Subscribers are now able to watch our live portfolios in real-time and fully validate them before risking capital.

In addition, for those who wish to implement their own investment ideas, we’ve established our Quant-for-Hire services by which our DAS (data analysis services) platform, along with our quants, can efficiently identify suitable data and quickly implement an investment idea. More specifically, our platform can backtest an investment approach historically, perpetually paper trade it, and ultimately deploy it for automated execution.

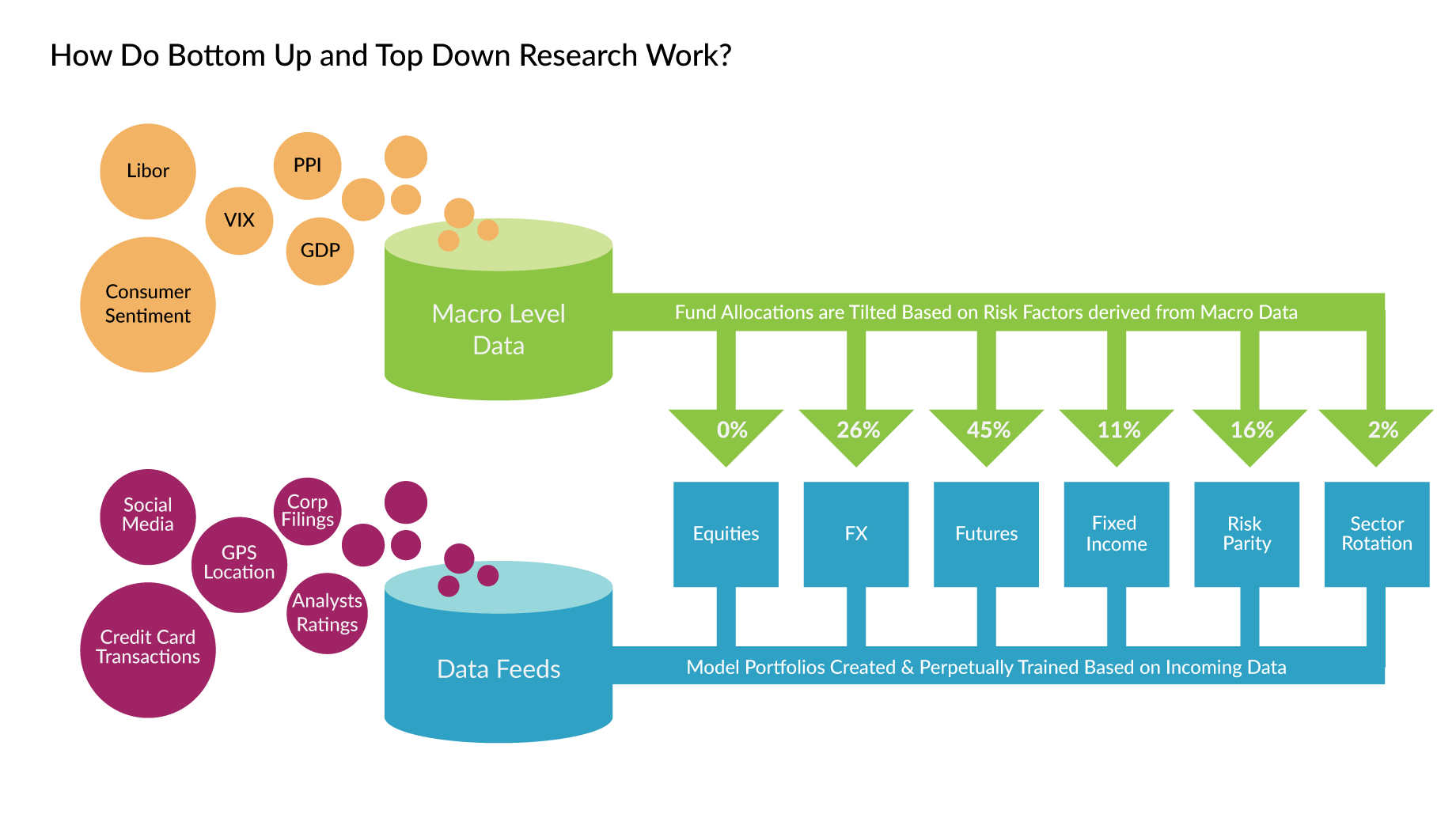

Image 1: A wide array of datasets empowering thematic uncorrelated model portfolios.

In the coming weeks I’d like to feature some of our portfolios. Today, I’d like to start with portfolios that exploit corporate events data sourced from Wall Street Horizon.

We’ve partnered with Wall Street Horizon in 2019 and launched two model portfolios:

Both portfolios assess how corporations publish events prior to their earnings dates. Using Wall Street Horizon’s accurate event data, we are able to build models that detect deviation from previous reporting protocols. For example, when corporations restate their upcoming earnings date, or publish ex-dividend dates, etc.

Our models are able to exploit how meaningful an event date relative to earnings date is, and further overlay additional fundamental, technical factors in order to identify optimal entry for either a short or a long outlook. The images below are of live traded portfolios (to be distinguished from backtests) and are available for real-time evaluations on our QuantDesk platform:

WSH Long Earnings: View backtest - View live: QuantDesk platform

Image 2: Wall Street Horizon Long Earnings has been traded live since March 2019. The portfolio has been able to consistently and meaningfully beat the S&P 500 in both absolute returns and Sharpe ratio. It also exhibits lower volatility with almost half the S&P’s max drawdown.

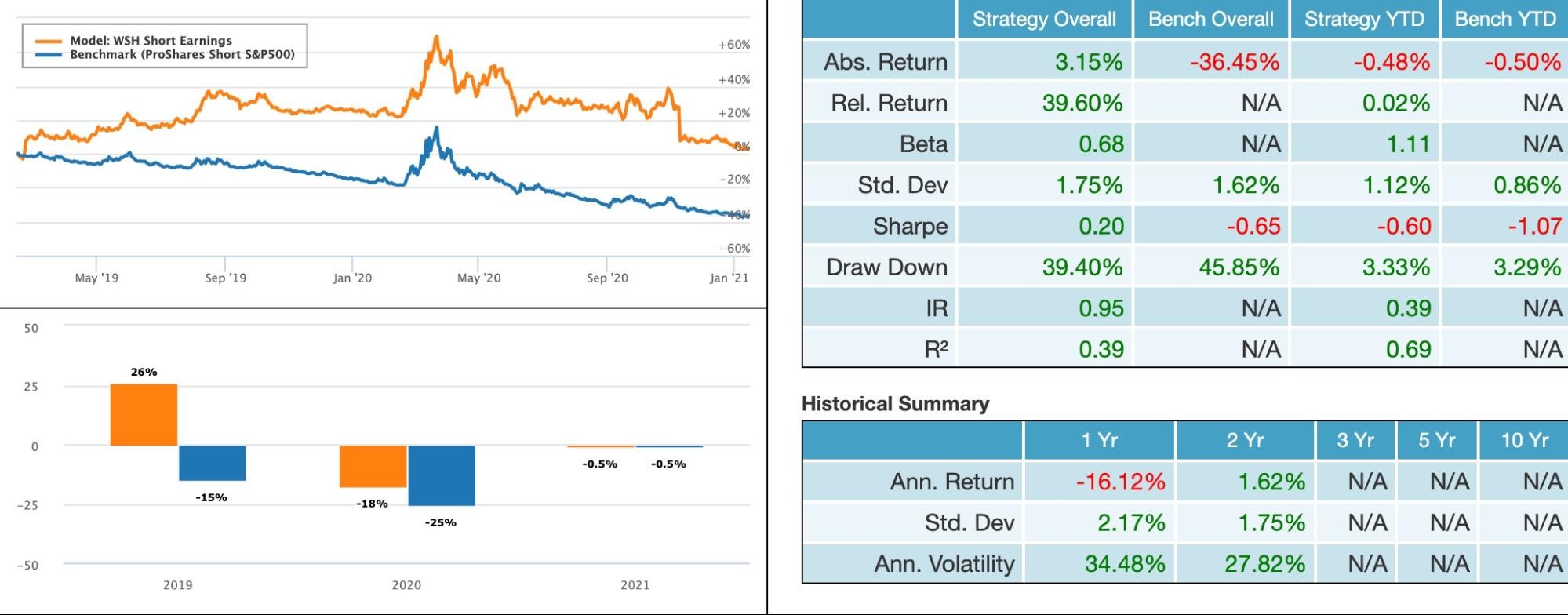

WSH Short Earnings: View backtest - View live: QuantDesk platform

Image 3: Wall Street Horizon Short Earnings has been traded live since February 2019.

Successful short-only portfolios are hard to come by and since markets tend to rise over time, they are mainly used as hedges vs stand alone investments.

The WSH Short Earnings portfolio is predicated on a model geared to identify unfavorable outlooks based on Wall Street Horizon corporate events data. For example, the portfolio identifies optimal conditions for entry when a company postpones its previously stated earnings date. As you can see, the portfolio was able to consistently beat its benchmark, SH (ProShares Short S&P500 ETF). In addition, it has been able to eke out positive returns even during the most bullish era the market has seen in years.

Next week, I will be covering another model portfolio based on extracting newsfeed sentiment from Benzinga financial news. We are now able to extract daily scoring on all news content pertaining to tradable assets using a sophisticated NLP (natural language processing) approach. Subsequently, we are able to deliver an exciting model portfolio for consumption.

If you are a data provider with unique data that could be useful for investment, we want to talk to you. In addition, if you are an investment professional looking for winning investment portfolios feel free to reach out to us. We’re happy to grant you trial access to a model portfolio that suits your investment style and mandate.

Erez M. Katz